Renewables are set to reach 46% of global electricity generation by 2030, with solar and wind driving most of the growth.

Global Growth Trends and Capacity Projections

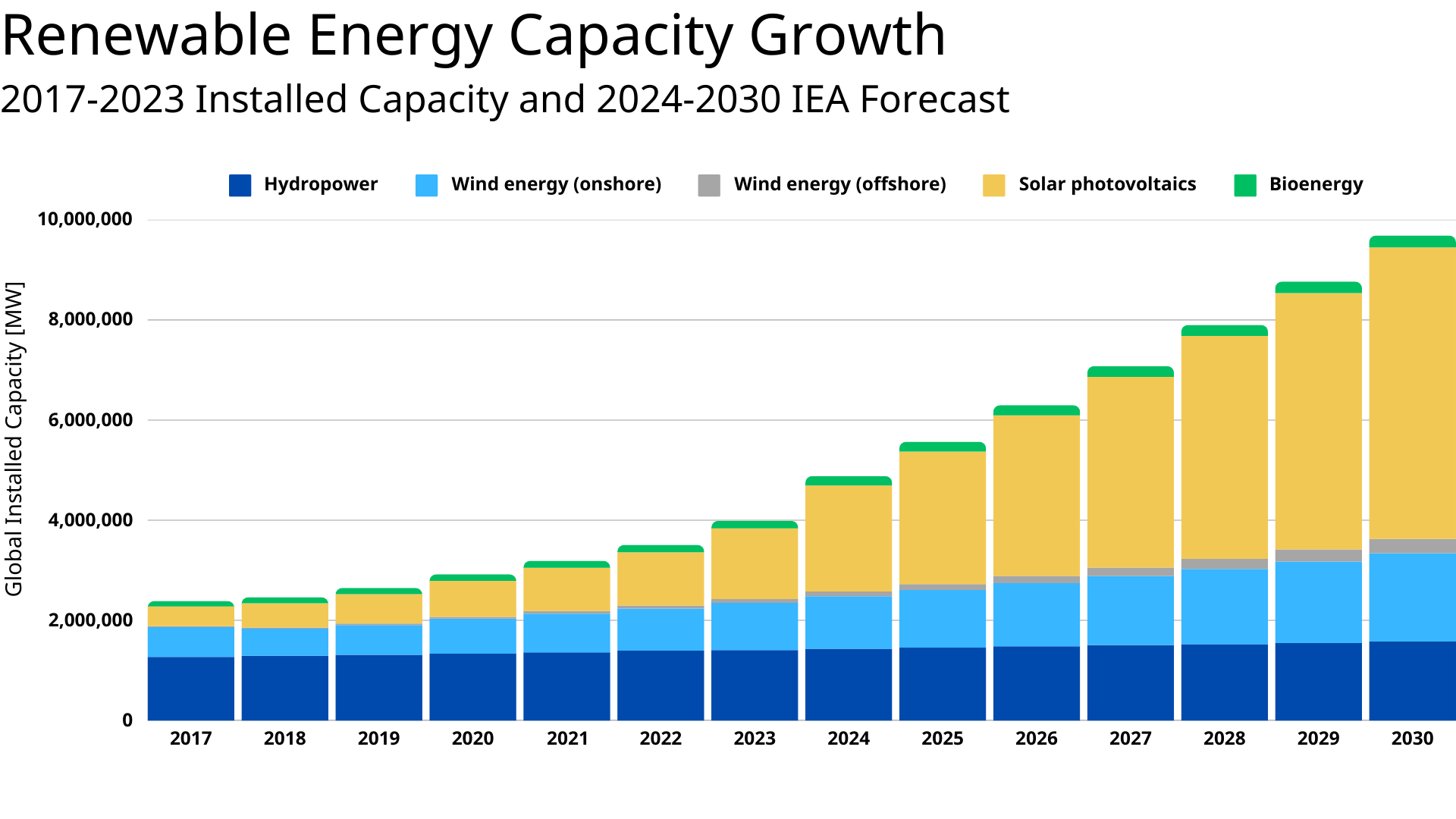

The world is projected to add 5,500 GW of new renewable energy capacity between 2024 and 2030—nearly tripling the additions seen between 2017 and 2023. This expansion will propel renewables to 46% of global electricity generation by 2030, up from 30% share in 2023.

Wind and solar are on track to double their existing contribution, rising from ~13% to 30% of global electricity generation by 2030. The share of renewables in final energy consumption is projected to expand from 13% in 2023 to nearly 20% by 2030.

There are two main actors in this story: solar photovoltaics and China.

▲ Fig 1 - Global Installed Capacity of Renewable Energy, 2014-2023, and 2024-2030 forecast. Source: IRENA, IEA

▲ Fig 1 - Global Installed Capacity of Renewable Energy, 2014-2023, and 2024-2030 forecast. Source: IRENA, IEA

Leading Technologies: Solar and Wind

Solar Photovoltaics

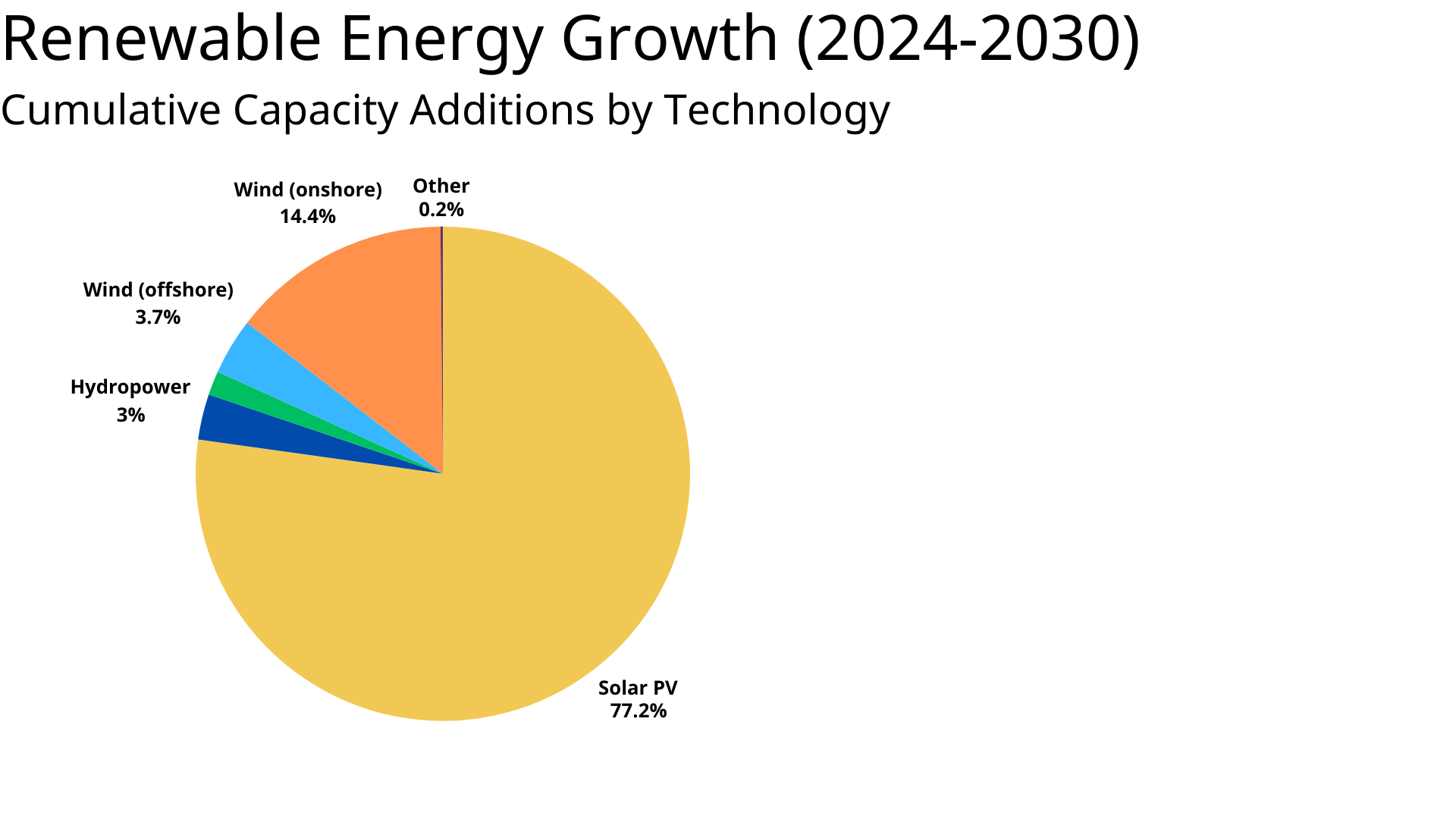

Solar PV is forecast to become the largest single source of renewable electricity by the end of the decade, overtaking both wind and hydropower. 80% of all new renewable energy capacity growth from now until 2030 will be solar.

This dominance is largely driven by falling costs of new solar installations. Solar remains the cheapest source of new electricity generation in almost every country.

Solar and wind will account for 95% of all new renewable energy installations between 2024 and 2030

Wind Energy

Wind power (onshore and offshore) is set to account for 15% of new capacity additions over the forecast period. The rate of expansion is expected to double between 2024 and 2030 compared with 2017–2023.

By 2030, wind is projected to surpass hydropower in electricity generation. However, supply chain bottlenecks (especially for offshore projects) and delayed permitting remain significant hurdles.

Together, solar PV and wind are expected to make up 95% of all renewable capacity growth by 2030.

By 2030, wind is projected to surpass hydropower in electricity generation

Other Renewables

The share of other renewables, including bioenergy, concentrated solar power and geothermal energy is projected to remain unchanged between 2023 and 2030 at less than 3% of global renewable electricity generation.

▲ Fig 2 - Renewable Energy Growth Forecast (2024-2030). Source: IEA

▲ Fig 2 - Renewable Energy Growth Forecast (2024-2030). Source: IEA

Regional Hotspots

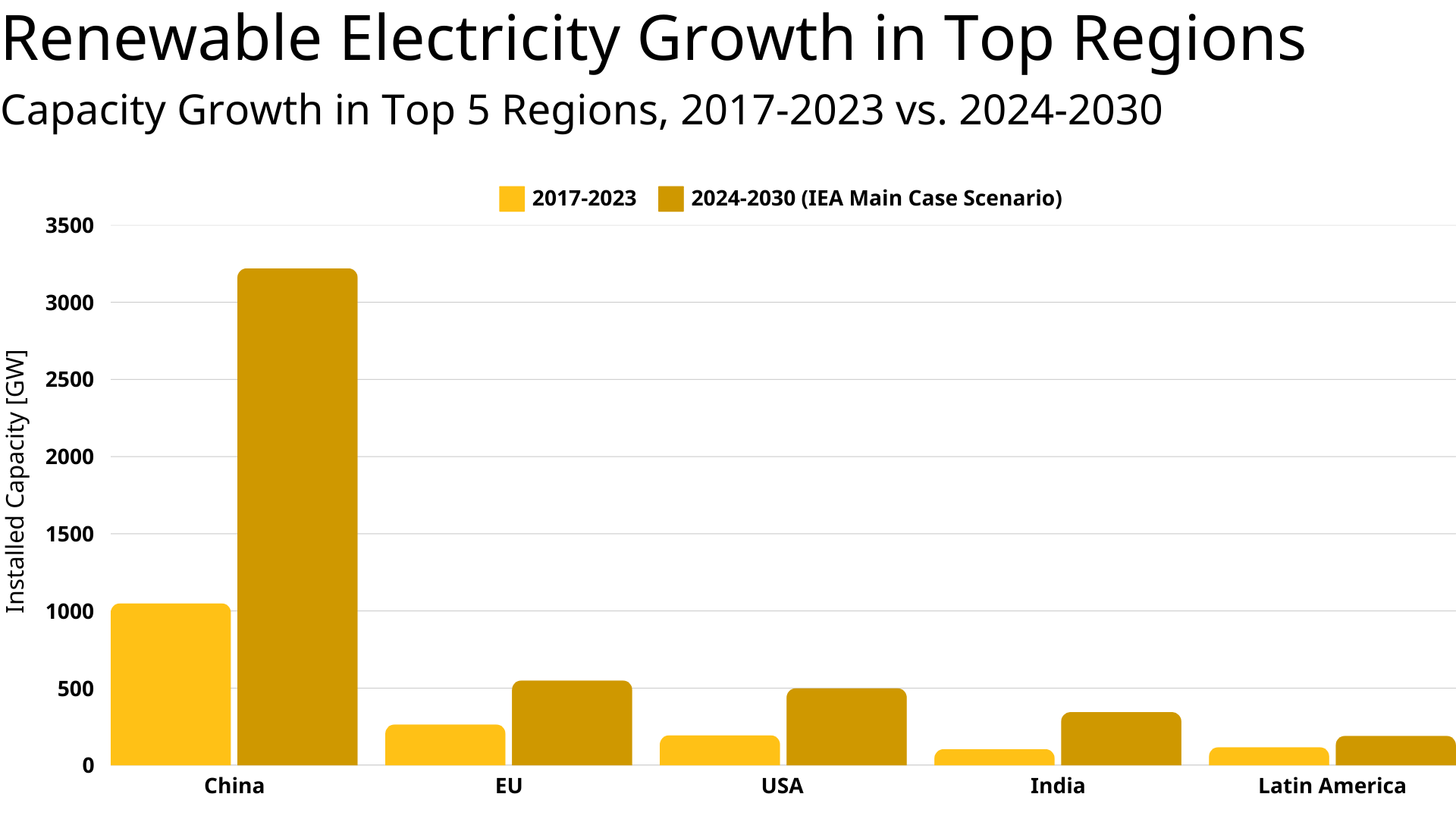

By 2030, China’s unprecedented expansion is expected to double its contribution to global renewable power output. Europe and the United States will account for almost 30% of global renewable power generation in 2030, followed by Brazil and India, which contribute another 5 percentage points each. Source: IEA

China

China is expected to install over 3,200 GW of new renewable electricity capacity between 2023 and 2030. which will account for 60% of global renewable capacity expansion by 2030. This will make China home to nearly half the world’s total renewable power capacity, up from a share of a third in 2010. China has already surpassed its 2030 solar and wind targets—six years ahead of schedule—and retains more than 80% of global PV manufacturing capacity.

High domestic demand, along with continued government support, ensures solar and wind projects in China stay cost-competitive. This concentration of manufacturing capacity in China of course means that any supply chain disruption in China (modules, inverters, raw materials) could ripple worldwide.

Europe and the United States

The European Union remains the second-largest growth market after China, with annual additions continuing to increase through 2030 at a faster pace than before.

The European Union and the United States are both forecast to double their pace of renewables additions between 2024 and 2030. Still, challenges like higher manufacturing costs for solar equipment and grid interconnection delays (especially in offshore wind) could constrain growth.

In EU member states, offshore wind expansion is at risk if new manufacturing projects and specialized vessel capacity fail to materialize.

India and Other Fast-Growth Markets

India stands out among large economies for its rapid scale-up in solar capacity. Meanwhile, nations like Chile, Germany, the Netherlands, and Portugal could reach nearly 70% wind and solar penetration by 2030.

▲ Fig 3 - Renewable Electricity Capacity Growth in Top 5 Regions (2017-2023 data, 2024-2030 estimate). Source: IEA

▲ Fig 3 - Renewable Electricity Capacity Growth in Top 5 Regions (2017-2023 data, 2024-2030 estimate). Source: IEA

Renewable Transport and Heat

Renewable energy extends beyond electricity generation into two major sectors: transport and heat. Renewable electricity is the primary source of renewable energy expansion in these two sectors.

Transport: 6% Renewable by 2030

Renewable fuels remain more expensive than fossil alternatives in transport. As a results, the share of renewables in that sector will only rise to about 6% by 2030.

This relatively slow adoption rate contrasts with the electricity sector’s growth, where plummeting costs of wind and solar drive market competitiveness. By comparison, transport fuels depend on more complex supply chains (refining biofuels, producing green hydrogen) and often require dedicated infrastructure such as charging stations. On top of that, vehicle turnover can be slow, meaning it takes years for new, more efficient vehicles to replace existing fleets, dragging down the transition.

Heat: 40% of Energy-Related Carbon Emissions

Heat accounts for almost half of global final energy consumption and contributes nearly 40% of energy-related $CO_2$ emissions today. While renewable heat consumption is forecast to grow by more than 50% (an increase of ~15 EJ) from 2024 to 2030, it still won’t keep pace with the overall rise in heat demand. This situation will lead to an estimated 5% increase in annual heat-related $CO_2$ emissions over the same period.

Solar thermal heat consumption in buildings is set to climb 40%, led by expansions in the Middle East (4× increase), China, and the EU. The EU alone makes up 6% of additional solar heat consumption but accounts for 75% of renewable district heating growth worldwide. This is enabled by new networks, fuel switching, and integration of diverse renewable sources (waste-to-energy, biomass co-firing, heat pumps, geothermal and solar thermal). With strong policy support through RED III targets, the EU is projected to reach 41% renewable district heat generation by 2030—far above the global average of 6%. Source: IEA

Expanding renewables by over 5.5 TW in just six years will require a massive workforce—translating into millions of new job opportunities.

Employment, Skills & Investment Needs

According to IRENA, the annual average investment in renewable power must reach USD 1,300 billion by 2030—up from USD 486 billion in 2022.

Additionally to substantial investments, expanding renewables by over 5.5 TW in six years will require a massive workforce. Solar and wind together are expected to account for roughly 95% of new capacity, translating into millions of fresh job opportunities across engineering, construction, project management, maintenance, and other specializations. According to estimates by industry analysts, a single gigawatt of newly installed solar capacity can create hundreds to thousands of direct and indirect jobs—particularly in manufacturing and installation. Meanwhile, the wind sector (onshore and offshore) increasingly needs project managers, turbine technicians, and offshore logistics experts to tackle rapid expansion.

Skilled workers in electrical engineering, automation, and software will of course be essential to managing complex power systems. A surge in new specialized roles is also anticipated: data analytics for predictive maintenance, AI-powered resource assessments, and real-time grid monitoring, and everything between and beyond. Things are moving fast.

At the same time, companies hire diverse talent with the soft skills needed for stakeholder engagement, negotiating land use, environmental permits, and community relations.

Challenges and Milestones

Policy Obstacles and Grid Bottlenecks

At least 1,650 GW of renewable capacity is in advanced stages but waiting for grid connection—up by 150 GW from last year. This is mainly due to to lagging infrastructure investment and complex permitting processes. Policy uncertainties—financing, permitting, social acceptance—still hinder faster deployment. Even so, 70 countries responsible for 80% of global renewable power capacity are on track to meet or exceed their current 2030 ambitions.

The 3xRenewables COP28 Target

During COP28, nearly 200 governments agreed to aim for “Tripling by 2030”—i.e., reaching about 11,000 GW of installed renewable capacity. Current forecasts show we’ll reach about 2.7 times the 2022 level by 2030, slightly shy of the 3x target. The Global Renewables Alliance collaborates with the International Renewable Energy Agency to track the progress on this target.

Still, the strong pace of renewables offers an opening for countries to update Nationally Determined Contributions (NDCs) in 2025 and aim even higher. “Renewables are moving faster than national governments can set targets for. This is mainly driven not just by efforts to lower emissions or boost energy security – it’s increasingly because renewables today offer the cheapest option to add new power plants in almost all countries around the world” remarked IEA Executive Director Fatih Birol.

Year-by-Year Milestones (2024–2030)

| Year | Milestone |

|---|---|

| 2024 | Solar PV and wind generation together surpass hydropower |

| 2025 | Renewables-based electricity overtakes coal |

| 2026 | Both wind and solar power generation exceed nuclear |

| 2027 | Solar PV generation surpasses wind |

| 2029 | Solar PV generation surpasses hydropower, becoming the largest renewable power source |

| 2030 | Wind-based generation surpasses hydropower |

▲ Table 1 - Expected Year-by-Year Milestones in Renewable Energy between 2023-2030. Source: International Energy Agency

By 2030, wind and solar will outpace hydropower, coal, and even nuclear in many key metrics. But progress in transport and heat lags behind renewable electricity development, leaving room for policy interventions and technological innovation.

Meanwhile, a shortage of skilled labor poses a real threat to the industry’s aggressive targets. Investment in grid infrastructure and workforce training must keep pace.

Looking for ways to join this transformative sector?

Explore Renewable Energy Roles on Rejobs.org - see how you can contribute to the global energy transition and build a rewarding career in wind, solar, and beyond.

References

- IEA Renewables 2024

- Global Renewables Alliance: 3xRE Tracking

- IRENA Digital Report – Tripling Renewable Power

- Global Energy Monitor: Wind & Solar Year in Review 2024

- IEA: The Energy World by 2030

- Statista: Share of electricity generation from wind and solar energy sources worldwide from 2010 to 2023

- IRENA: Renewable Energy and Jobs – Annual Review 2024.

Article by Jaroslav Holub · Edited by the Rejobs Editorial Team

Published on February 19, 2025

Share this blog post with anyone who might be looking for a career in renewable energy.